Quick answer: San Diego property values are driven by supply, local demand, rates, and incomes — not by national headlines written to get clicks. The disciplined read: stop forecasting from news cycles, watch local inventory and absorption, and make buy/hold decisions on structure and cash flow. This is education and analysis, not financial advice.

- Why are real-estate headlines usually wrong for you?

- What actually moves San Diego property values?

- Why don’t national numbers describe San Diego?

- How do interest rates really affect prices?

- What do past San Diego cycles teach?

- How do you read the local market without the noise?

- How should this change your buy or hold decision?

- Is waiting for a crash a strategy?

- What headline-driven mistakes cost the most?

- Frequently asked questions

Why are real-estate headlines usually wrong for you?

National real-estate headlines are written for clicks across an entire country, not for a decision on one home in one San Diego submarket. They optimize for attention, while your decision needs local, specific, time-stamped data that a national story almost never contains.

As a San Diego broker, MBA, and former corporate banker, I treat headlines the way a banker treats market chatter: signal to be filtered, never an input to a position. The disciplined alternative is the same one in our capital-allocation guide — decide on structure, not sentiment.

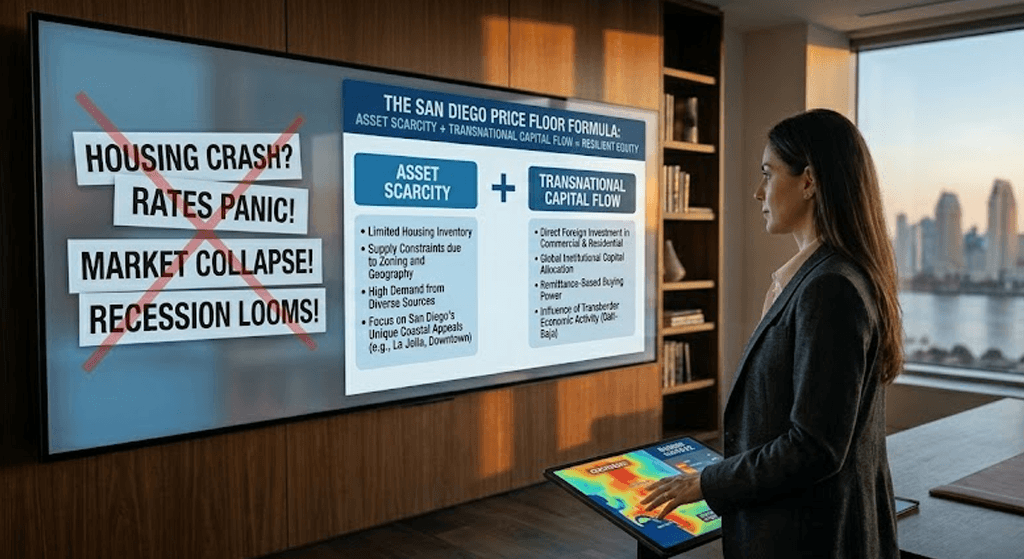

What actually moves San Diego property values?

Local prices are set by a few durable forces, and headlines rarely measure any of them accurately:

- Supply — San Diego is structurally supply-constrained, which supports prices through cycles.

- Local demand — jobs, migration, and bilingual cross-border demand.

- Financing cost — rates change affordability and buyer-pool size.

- Incomes — what local buyers can actually sustain.

Watch these and the market becomes legible. Watch headlines and it becomes random noise you cannot act on with any confidence.

Why don’t national numbers describe San Diego?

A national median can fall while a supply-constrained coastal market holds or rises, because they are different markets with different supply and demand. Applying a U.S.-wide statistic to a San Diego neighborhood is a category error, not analysis.

Real estate is local down to the boundary — the same reason a school zone moves price in our Carmel Valley buyer guide. The right unit of analysis is the submarket, not the country, and rarely even the metro.

How do interest rates really affect prices?

Rates change monthly affordability and the size of the active buyer pool, but in a supply-constrained market they often compress transaction volume more than price. Fewer buyers can still meet limited inventory, which is why “rates up, prices crash” frequently fails locally.

The honest framing: rates affect what you pay monthly and your competition, not a guaranteed price direction. Decisions should be built on your numbers at today’s rate, not a prediction of tomorrow’s — you can refinance a rate, but you cannot refinance a missed entry.

What do past San Diego cycles teach?

Across multiple cycles, supply-constrained coastal markets have tended to fall less and recover faster than the national average, because limited inventory puts a floor under demand even when sentiment turns negative. The lesson is not “prices only go up” — it is that local structure, not the headline of the moment, sets the depth and length of a downturn.

Owners who were forced to sell in a downturn took the loss; owners who had structured for liquidity and cash flow waited it out and kept the asset. The difference was never the forecast — it was preparation, which is the only variable you actually control.

How do you read the local market without the noise?

Replace headlines with a short, repeatable local dashboard:

| Signal | What it tells you |

|---|---|

| Active + pending inventory | Real current competition |

| Absorption rate (months of inventory) | Direction and pace |

| Price-cut frequency | Seller pressure |

| Days on market trend | Demand strength now |

Four local numbers, checked monthly, beat a year of national headlines for any real decision you have to make.

How should this change your buy or hold decision?

The decision stops being “what will the market do” and becomes “do the numbers work for me, at today’s rate, in this submarket.” That question is answerable; the forecast is not.

Underwrite on stressed cash flow and a designed exit, exactly as in our guide to real estate as a liquid asset and, for investors, sheltering capital in San Diego property. Structure survives forecasts being wrong.

Is waiting for a crash a strategy?

Waiting for a predicted crash is a forecast, not a strategy, and forecasts have a poor record in supply-constrained markets. The measurable cost of waiting — rent paid, equity not built, and a possibly higher entry later — is usually ignored in the headline that prompted the wait.

A strategy has defined triggers and numbers; “wait and see” has neither. That distinction is the entire point of analysis over anxiety.

What headline-driven mistakes cost the most?

The expensive ones: applying national stats to a local decision, timing the market on rate predictions, waiting indefinitely for a forecast crash, and ignoring local inventory data that was available the whole time. Each substitutes a story for analysis.

Frequently asked questions

Are San Diego home prices going to crash?

No one can forecast that reliably, and supply constraints have historically resisted crashes. The useful approach is watching local inventory and absorption, not predicting a national event.

Do national real-estate headlines apply to San Diego?

Often not. A national median can fall while a supply-constrained coastal submarket holds or rises — they are different markets with different drivers.

Should I wait for interest rates to drop before buying?

Rates affect monthly cost and competition, not a guaranteed price direction. Decide on your numbers at today’s rate; you can refinance a rate, not a missed entry.

What data should I actually watch?

Local active and pending inventory, absorption rate, price-cut frequency, and days-on-market trend — checked monthly for your specific submarket.

Is waiting for a crash a safe choice?

It is a forecast, not a strategy, and it carries real costs — rent paid, equity not built, possible higher entry later — that headlines rarely mention.

This article is educational market analysis, not financial or investment advice. Market conditions change; verify current local data and consult qualified professionals before making a real-estate decision.

Decide on data, not headlines

Najla Wehbe Dipp — San Diego real estate broker (eXp Realty, CA DRE #02024371), MBA and former corporate banker — gives buyers and investors an uncensored, data-driven read of the San Diego market. Bilingual (English/Spanish).

📞 Call 858-333-2455 ✉️ Send a message 📍 Visit our contact page